Chasing the (structural budget deficit) Ball Downhill

Stein’s Law – If something cannot go up forever. It will stop.

Hopefully, in this age of video games and mindless scrolling, there are still lots of kids who get bored enough that they have no other option but to go outside, find a sibling or a friend and make up a game. Years ago, my kids invented a game they called “Road Tennis”, which is basically tennis with lines spray painted on the street and the curb serves as the side boundary. Instead of a net, the ball had to clear the width of the driveway, which became known as the “dreaded zone of death”. Many, many hours have been spent playing road tennis in front of my house. While the road out front is pretty flat, it starts to descend into a long hill just past the driveway. That meant that whoever was the road tennis competitor on the downhill side had to remain vigilant to never let any ball, whether in or out, get past them. Not only was there the exhausting chore of chasing the ball downhill, but there was also the risk that the ball would make it all the way to the storm drain which might mean the end of the game.

Chasing a ball downhill is how it will feel when some future President and Congress are given no choice but to attempt fiscal credibility. Why? Because taking away the punchbowl of fiscal stimulus risks slower growth and therefore less taxes to be collected. Additionally, this issue is compounded by the trends of aging demographics, a collapse in immigration, upward pressure on defense spending and a US economy likely to grow more slowly, but still experience higher inflation volatility and thereby higher interest costs.

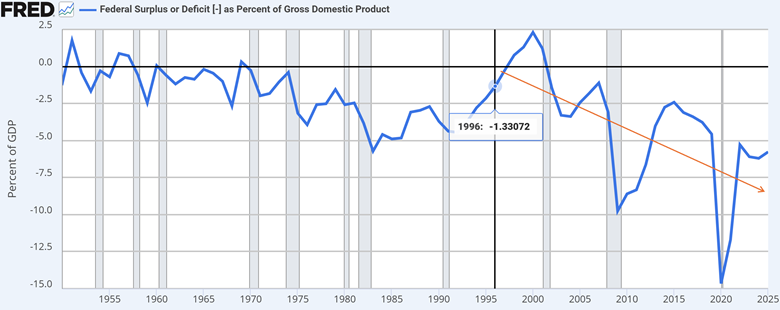

The chart above depicts budget deficits and a brief surplus since 1950. What is clear from the chart is that despite a strong economy, a sixteen-year bull market in stocks and a historically low unemployment rate, the US has become addicted to deficits. Since WW2, deficits invariably rose with unemployment and shrank when labor markets tightened. That is no longer the case. Our deficits are now structurally high despite an optimal environment for federal revenues. Consider what might the deficit look like in a recession, 8%? Maybe 9%?

In the early days of the current administration, Treasury Secretary Scott Bessent argued that we could achieve 3% real (excluding inflation) growth, while cutting deficits down to 3% of GDP. As last year progressed, those arguments were abandoned. Real Growth has been less than 3% and deficits are still running at about 6% with an upward trend for 2026. The problem, as Mr. Bessent knows, is that had we cut spending or raised taxes adequately to even target 3% deficits, there is broad agreement among economists that growth would have materially slowed. Once the excess spending is embedded, taking it away is really hard.

We spend roughly $1T on defense annually. In a world where the US is no longer the singular hegemonic power, is that number likely to rise or fall? The President has said that he thinks the defense budget should be 50% higher. That won’t happen but the trend is clear. Rising defense spending crowds out other spending that is more immediately stimulative to the economy.

Demographics are, at this point, a well-understood and well-documented issue. This isn’t the 1950’s when 90% of American men were in the labor force. We are entering a period of rapidly accelerating retirements as the baby boomers exit the workforce. We have an economic system where the productivity of younger Americans subsidize the retirements of older Americans. With birth rates inexorably falling, that arrangement puts a greater burden on a smaller number of workers relative to the number of retirees. Exacerbating that mismatch is the collapse in immigration. In February, the conservative leaning Cato Institute published a study that concluded: “The fiscal surplus from all immigrants from 1994 to 2023 was $14.5 trillion, compared with a deficit of $48 trillion without immigrants. That means that immigrants cut deficits by nearly a third in real terms over the last three decades.” In other words, if we continue to prevent immigration, our fiscal situation is likely to rapidly deteriorate, hastening the pressure on Congress and a US President.

I get it. The Cassandras have been crying and warning of the impending doom of excessive debt and deficits for a long time and yet the crisis has never materialized. But never in the past have we had the confluence of factors that we have today. Ultimately, it will be the bond market that forces the hand of policymakers. It will not be until the yield curve steepens sharply that US politicians will have the political cover and incentive to address deficits. It is not until fiduciaries globally decide they no longer want to incur the duration risk of profligate borrower. When they do, the solution will be economically painful and potentially, the ball makes it to the storm drain in the form of dollar devaluation and higher structural inflation.

WealthVest makes no representation or warranty, expressed or implied, with respect to the accuracy, reasonableness, or completeness of any of the statements made in this material, including, but not limited to, statements obtained from third parties. Opinions, estimates and projections constitute the current judgment of Tim as of the date indicated. They do not necessarily reflect the views and opinions of WealthVest and are subject to change at any time without notice. WealthVest does not have any responsibility to update this material to account for such changes. There can be no assurance that any trends discussed during this material will continue.

Statements made in this material are not intended to provide, and should not be relied upon for, accounting, legal or tax advice and do not constitute an investment recommendation or investment advice. Investors should make an independent investigation of the information discussed in this material, including consulting their tax, legal, accounting or other advisors about such information. WealthVest does not act for you and is not responsible for providing you with the protections afforded to its clients. This material does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product or service, including interest in any investment product or fund or account managed or advised by WealthVest.

Certain statements made in this material may be “forward-looking” in nature. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. As such, undue reliance should not be placed on such statements. Forward-looking statements may be identified by the use of terminology including, but not limited to, “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

The S&P 500® is a trademark of Standard & Poor’s Financial Services, LLC and its affiliates and for certain fixed index annuity contracts is licensed for use by the insurance company producer, and the related products are not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC or their affiliates, none of which make any representation regarding the advisability of purchasing such a product. WealthVest is not affiliated with, nor does it have a direct business relationship with Standard & Poors Financial Services, LLC.